Inflation and Monetary Policy: Key Insights

How Interest Rates Influence Inflation

Understanding how interest rates affect inflation can empower you to make smarter financial decisions—whether you’re saving for a home, managing debt, or planning for retirement. At its core, inflation refers to the general rise in prices over time, which reduces the purchasing power of your money. Central banks, like the Federal Reserve in the U.S., use interest rates as a key tool to control inflation.

When inflation is high, central banks often raise interest rates. This makes borrowing more expensive and saving more attractive. As a result, people and businesses tend to spend less, which slows down economic activity and helps bring inflation under control. On the flip side, when inflation is low or the economy is sluggish, central banks may lower interest rates to encourage borrowing and spending, which can stimulate growth.

So, why does this matter to you? Because interest rates influence everything from mortgage payments and credit card interest to the returns on your savings account. By keeping an eye on interest rate trends, you can better time big purchases, adjust your investment strategy, and protect your financial well-being.

In short, interest rates and inflation are closely linked. Understanding this relationship can help you stay ahead financially and make more informed choices in your everyday life.

Monetary Policy Tools and Their Impact

Understanding how central banks manage inflation and economic stability can empower you to make smarter financial decisions. One of the key ways they do this is through monetary policy tools. These tools help control the money supply, influence interest rates, and ultimately impact inflation, employment, and economic growth.

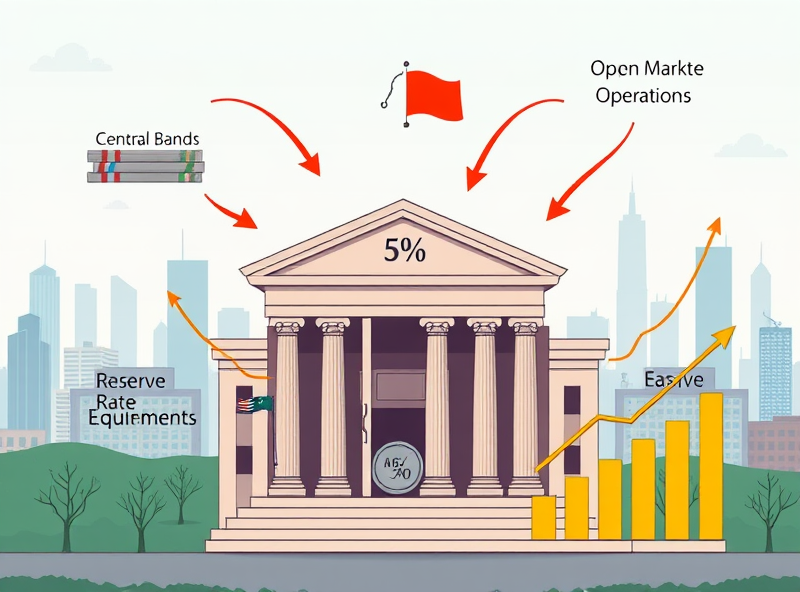

The main tools of monetary policy include:

1. Open Market Operations (OMO): This involves the buying and selling of government securities in the open market. When a central bank buys securities, it injects money into the economy, encouraging spending and investment. Selling securities does the opposite, helping to cool down inflation.

2. Interest Rate Policy: Central banks, like the Federal Reserve, adjust the benchmark interest rate (such as the federal funds rate in the U.S.) to influence borrowing and lending. Lower interest rates make loans cheaper, boosting spending and investment. Higher rates help reduce inflation by making borrowing more expensive.

3. Reserve Requirements: This is the minimum amount of reserves that banks must hold. Lowering reserve requirements increases the money banks can lend, stimulating the economy. Raising them restricts lending, helping to curb inflation.

4. Quantitative Easing (QE): In times of economic downturn, central banks may purchase longer-term securities to increase money supply and encourage lending and investment.

Each of these tools has a ripple effect on everyday life. For example, when interest rates are low, mortgage rates tend to drop, making homeownership more affordable. On the other hand, higher rates can increase credit card and loan payments, encouraging people to save more and spend less, which helps control inflation.

By understanding these tools, you can better anticipate economic trends and make informed decisions about saving, investing, or borrowing. Staying informed about monetary policy isn’t just for economists—it’s a practical way to navigate your financial future with confidence.

U.S. Inflation Trends and Policy Effects

Understanding how inflation behaves in the U.S. and how monetary policy responds to it can help us all make smarter financial decisions. Over the past few years, inflation in the United States has experienced significant fluctuations—rising sharply during the pandemic due to supply chain disruptions and increased consumer demand, and more recently, showing signs of moderation as the Federal Reserve raised interest rates.

When inflation rises, the Federal Reserve typically increases interest rates to cool down the economy. This makes borrowing more expensive, which slows down spending and investment, ultimately helping to bring inflation back under control. On the other hand, when inflation is low or the economy is slowing, the Fed may lower interest rates to encourage growth.

The recent rate hikes by the Fed have started to show their effects. Consumer price increases have begun to ease, especially in areas like energy and used cars. However, core inflation—excluding food and energy—remains sticky, suggesting that the policy effects take time to fully materialize.

For everyday people, understanding these trends is empowering. If you’re planning to buy a home, take out a loan, or invest, knowing where inflation and interest rates are headed can help you time your decisions better. It’s also a reminder to stay flexible with your financial plans and to keep an eye on economic indicators.

In short, inflation and monetary policy are deeply connected. By staying informed, you can better protect your purchasing power and make choices that support your long-term financial well-being.

The Taylor Rule and Strategic Rate Setting

Understanding how central banks set interest rates can help us all make better financial decisions—whether you’re a homeowner, investor, or just trying to manage your savings. One key tool economists and policymakers use is the Taylor Rule. This simple yet powerful formula helps guide central banks in adjusting interest rates based on two main factors: inflation and the output gap (the difference between actual and potential economic output).

The Taylor Rule suggests that when inflation rises above the target (usually around 2%), central banks should raise interest rates to cool down the economy. Conversely, if inflation is too low or the economy is underperforming, interest rates should be lowered to stimulate growth. This rule provides a structured and transparent way to think about monetary policy, which can help reduce uncertainty in financial markets.

By following the Taylor Rule, central banks aim to strike a balance—keeping inflation in check while supporting economic growth. For individuals, understanding this can offer valuable insight into where interest rates might be headed, helping you plan for things like mortgage rates, savings yields, or investment returns.

So next time you hear about the Federal Reserve or another central bank adjusting rates, remember the Taylor Rule—it’s a guiding light in the complex world of monetary policy.

답글 남기기